Navigating the 2026 Housing Market: Smart Financing for First-Time Buyers

Navigating the 2026 Housing Market: Smart Financing Strategies for First-Time Buyers

The dream of homeownership remains a cornerstone of the American ideal, a symbol of stability, personal achievement, and a significant investment in one’s future. For first-time buyers, however, the path to purchasing a home can often seem daunting, especially in an ever-evolving landscape like the 2026 housing market. With economic shifts, fluctuating interest rates, and varying inventory levels, understanding the nuances of the market and, crucially, mastering smart financing strategies are paramount.

This comprehensive guide is designed to empower first-time buyers, providing them with the knowledge and tools necessary to confidently navigate the complexities of the 2026 housing market. We’ll delve into the projected trends, explore diverse financing options, and offer actionable advice to help you secure your dream home without falling into common pitfalls. Whether you’re just starting to save or actively searching, preparing yourself with robust financial strategies will be your greatest asset.

Understanding the 2026 Housing Market Landscape

Before diving into financing, it’s essential to grasp the potential state of the 2026 housing market. While predictions are inherently speculative, experts base their forecasts on current economic indicators, demographic shifts, and historical trends. Understanding these factors will help you set realistic expectations and tailor your purchasing strategy accordingly.

Key Factors Influencing the Market

- Interest Rates: Mortgage interest rates are a critical determinant of affordability. While they have seen volatility in recent years, the 2026 outlook will largely depend on inflation, Federal Reserve policies, and global economic stability. Higher rates mean higher monthly payments, impacting buying power.

- Housing Inventory: The supply of available homes significantly affects prices. A low inventory often leads to bidding wars and higher prices, while an increase in supply can create a more balanced or even buyer-friendly market. Construction rates and existing home sales will be key indicators.

- Economic Growth and Employment: A strong economy with robust job growth typically supports a healthy housing market, as more people have the financial stability to purchase homes. Conversely, economic slowdowns can dampen demand.

- Demographic Shifts: The millennial generation, now reaching prime home-buying age, continues to be a driving force in the housing market. Their preferences for location, home size, and amenities will shape demand in various regions.

- Inflation: Persistent inflation can lead to higher interest rates and increased costs for construction materials, potentially impacting both new home prices and the overall cost of living, which in turn affects affordability.

Projected Trends for First-Time Buyers in 2026

For first-time buyers, the 2026 housing market might present a mixed bag of opportunities and challenges. Some analysts anticipate a gradual normalization, moving away from the extreme highs and lows seen in previous years. This could mean:

- Moderated Price Growth: While significant price drops are unlikely in most stable markets, the rapid appreciation rates of the past might slow down, offering more predictable pricing.

- Increased Inventory (Potentially): If construction continues to pick up and homeowners become more willing to sell, the inventory squeeze might ease slightly, giving buyers more options.

- Continued Competition in Desirable Areas: Even with more inventory, high-demand urban and suburban areas are likely to remain competitive, requiring buyers to be well-prepared and act swiftly.

- Importance of Financial Prudence: Regardless of market conditions, a strong financial foundation will be crucial. Lenders will continue to scrutinize creditworthiness, income stability, and debt-to-income ratios.

Building Your Financial Foundation: The Cornerstone of Homeownership

Before you even start browsing listings, establishing a solid financial foundation is the most critical step for any first-time buyer in the 2026 housing market. This involves more than just saving for a down payment; it encompasses credit health, debt management, and a realistic understanding of ongoing homeownership costs.

1. Credit Score: Your Financial Passport

Your credit score is arguably the most important number in your home-buying journey. It dictates the interest rate you’ll qualify for, directly impacting your monthly mortgage payments and the total cost of your loan. Lenders use FICO scores, generally requiring a minimum score of 620 for conventional loans, though higher scores (740+) unlock the best rates.

- Check Your Credit Report: Obtain free copies of your credit report from Equifax, Experian, and TransUnion annually at AnnualCreditReport.com. Review them for errors and discrepancies.

- Pay Bills on Time: Payment history is the largest factor in your credit score. Set up automatic payments to avoid missing due dates.

- Reduce Debt: High credit utilization (the amount of credit you use compared to your total available credit) can negatively impact your score. Pay down credit card balances and other revolving debt.

- Avoid New Credit: Refrain from opening new credit accounts or making large purchases on credit before and during the home-buying process, as this can temporarily lower your score.

2. Saving for a Down Payment and Closing Costs

The down payment is often the biggest hurdle for first-time buyers. While 20% is traditionally recommended to avoid private mortgage insurance (PMI), many loan programs allow for much lower down payments. However, a larger down payment generally means a smaller loan, lower monthly payments, and less interest paid over the life of the loan.

- Down Payment: Aim for as much as you can comfortably afford. Even 5-10% can make a significant difference. Explore down payment assistance programs (discussed later).

- Closing Costs: These are fees associated with the home purchase, typically ranging from 2% to 5% of the loan amount. They include appraisal fees, title insurance, legal fees, and loan origination fees. Budget separately for these; they are in addition to your down payment.

- Emergency Fund: Beyond the down payment and closing costs, having an emergency fund (3-6 months of living expenses) is crucial for unexpected home repairs or financial setbacks. Homeownership comes with ongoing maintenance costs.

3. Budgeting and Debt-to-Income Ratio (DTI)

Lenders assess your ability to repay a loan by looking at your DTI ratio. This compares your total monthly debt payments to your gross monthly income. Most lenders prefer a DTI of 36% or lower, though some may go up to 43% or even 50% for certain loan types.

- Calculate Your DTI: Sum up all your monthly debt payments (credit cards, car loans, student loans, etc.) and divide by your gross monthly income.

- Reduce Non-Essential Spending: Cut back on discretionary expenses to free up more money for savings and debt repayment.

- Increase Income: Explore opportunities for side hustles or salary negotiations to boost your monthly income, which can improve your DTI and accelerate savings.

Smart Financing Strategies for the 2026 Housing Market

Once your financial foundation is solid, it’s time to explore the diverse financing options available. The 2026 housing market will likely offer a range of loan products, and understanding which one best suits your situation can save you thousands of dollars and simplify your home-buying journey.

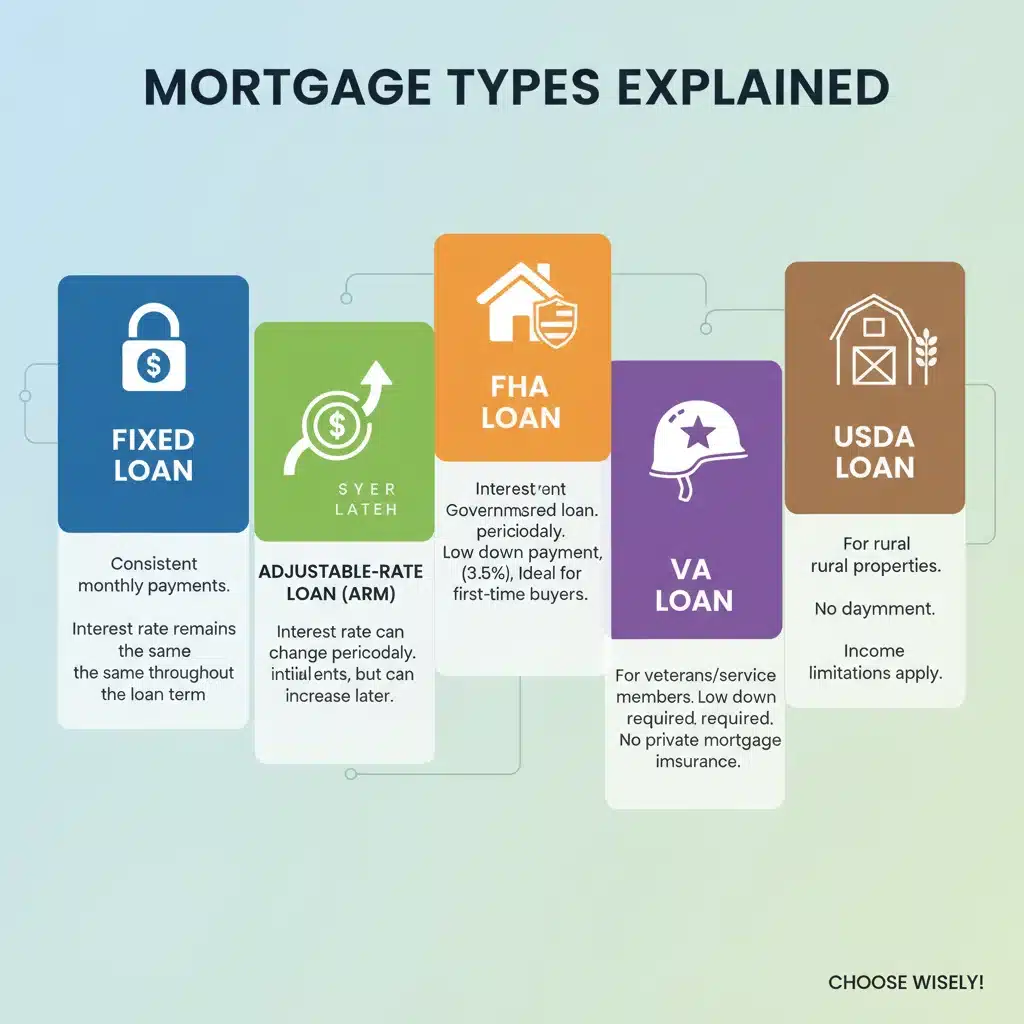

1. Conventional Loans

These are the most common type of mortgage and are not insured or guaranteed by a government agency. They often require good to excellent credit. If you put down less than 20%, you’ll typically need to pay Private Mortgage Insurance (PMI) until you reach 20% equity.

- Pros: Flexible terms, can be used for various property types, PMI can eventually be removed.

- Cons: Stricter credit requirements, higher down payment often preferred.

2. Government-Backed Loans: A Boon for First-Time Buyers

These loans are often ideal for first-time buyers due to their more lenient requirements.

FHA Loans (Federal Housing Administration)

FHA loans are insured by the government, making them less risky for lenders. This allows for lower credit score requirements and down payments as low as 3.5%.

- Pros: Low down payment, more flexible credit requirements, competitive interest rates.

- Cons: Requires upfront and annual mortgage insurance premiums (MIP) for the life of the loan (unless you put down 10% or more, then it’s 11 years).

VA Loans (Department of Veterans Affairs)

Available to eligible service members, veterans, and surviving spouses, VA loans are one of the most powerful financing tools. They often require no down payment and no private mortgage insurance.

- Pros: 0% down payment, no PMI, competitive interest rates, limited closing costs.

- Cons: Eligibility restrictions, requires a VA funding fee (unless exempt).

USDA Loans (U.S. Department of Agriculture)

These loans are designed for low-to-moderate-income buyers in eligible rural and some suburban areas. They also offer 0% down payment options.

- Pros: 0% down payment, low monthly mortgage insurance.

- Cons: Strict income limits, property must be in an eligible rural area.

3. Adjustable-Rate Mortgages (ARMs) vs. Fixed-Rate Mortgages

The choice between an ARM and a fixed-rate mortgage is crucial, especially in a dynamic 2026 housing market.

- Fixed-Rate Mortgage: Your interest rate and monthly principal and interest payments remain the same for the life of the loan (e.g., 15 or 30 years). Provides stability and predictability.

- Adjustable-Rate Mortgage (ARM): The interest rate is fixed for an initial period (e.g., 5, 7, or 10 years), and then it adjusts periodically based on a market index. Can offer lower initial payments but carries the risk of higher payments later. Consider an ARM if you plan to move or refinance before the fixed period ends.

4. First-Time Home Buyer Programs and Assistance

Many states, counties, and cities offer programs specifically designed to help first-time buyers overcome financial hurdles. These can include:

- Down Payment Assistance (DPA): Grants or low-interest loans to help cover your down payment and/or closing costs. Some are forgivable after a certain period if you remain in the home.

- Mortgage Credit Certificates (MCCs): Allow you to claim a portion of your annual mortgage interest as a dollar-for-dollar tax credit, reducing your federal income tax liability.

- Reduced Interest Rate Programs: Some programs offer lower-than-market interest rates for eligible buyers.

Research programs available in your specific area. Websites of your state’s housing finance agency (HFA) are excellent resources.

The Pre-Approval Process: Your Competitive Edge

In the competitive 2026 housing market, being pre-approved for a mortgage is not just a formality; it’s a strategic advantage. Pre-approval means a lender has reviewed your financial information (income, credit, assets) and committed to lending you a specific amount, subject to the property appraisal and other conditions.

- Know Your Budget: Pre-approval clearly defines how much you can afford, preventing you from looking at homes outside your price range.

- Strengthen Your Offer: Sellers often prefer offers from pre-approved buyers, as it signals you are serious and financially capable, making your offer more attractive.

- Streamline the Process: Having your financial documents already reviewed speeds up the underwriting process once you find a home.

It’s important to distinguish pre-approval from pre-qualification. Pre-qualification is a preliminary estimate based on self-reported information, while pre-approval involves a more thorough verification of your finances.

Beyond the Mortgage: Hidden Costs and Long-Term Planning

Many first-time buyers focus solely on the mortgage payment, but homeownership comes with a host of other expenses that must be factored into your budget, especially when planning for the 2026 housing market.

Ongoing Homeownership Costs

- Property Taxes: These vary significantly by location and are a recurring expense.

- Homeowners Insurance: Mandatory to protect your investment against damage, theft, and liability. Flood and earthquake insurance may be additional depending on your area.

- Utilities: Budget for electricity, gas, water, sewer, trash, internet, and cable. These can be higher than renting, especially in larger homes.

- Maintenance and Repairs: Experts recommend setting aside 1-3% of your home’s value annually for maintenance. This covers everything from routine upkeep (lawn care, HVAC servicing) to unexpected repairs (roof leaks, appliance breakdowns).

- HOA Fees: If you buy a condo, townhouse, or a home in a planned community, you’ll likely pay Homeowners Association (HOA) fees, which cover shared amenities and common area maintenance.

Refinancing and Equity Building

Homeownership is also about building equity, which is the portion of your home that you own outright. As you pay down your mortgage and as your home’s value appreciates, your equity grows. This equity can be a valuable asset in the future.

- Refinancing: If interest rates drop significantly after you purchase your home, or if your credit score improves, you might be able to refinance your mortgage to a lower rate, reducing your monthly payments or the total interest paid.

- Home Equity Loans/Lines of Credit: Once you’ve built substantial equity, you can borrow against it through a home equity loan or a home equity line of credit (HELOC) for major expenses like renovations or education.

Expert Tips for First-Time Buyers in the 2026 Housing Market

Beyond the financial mechanics, several strategic tips can help first-time buyers succeed in the 2026 housing market.

1. Work with a Reputable Real Estate Agent

A good agent is your advocate. They understand local market conditions, can help you find suitable properties, negotiate on your behalf, and guide you through the complex paperwork. Interview several agents to find one who aligns with your needs and communication style.

2. Don’t Waive Contingencies Hastily

In a competitive market, buyers sometimes waive contingencies (like inspections or appraisals) to make their offer more attractive. While this can be tempting, it carries significant risks. A home inspection can uncover costly issues, and an appraisal contingency protects you if the home’s value is less than the offer price.

3. Be Patient and Flexible

Finding the right home takes time. The 2026 housing market might still require patience. Be prepared to view multiple properties and possibly make several offers. Flexibility on location, home size, or move-in dates can also open up more opportunities.

4. Consider All-In Costs, Not Just Price

When evaluating homes, think about the total cost of ownership. A slightly cheaper home might have higher property taxes, HOA fees, or require extensive renovations, making it more expensive in the long run. Factor in potential utility costs based on the home’s age and energy efficiency.

5. Get Multiple Loan Quotes

Don’t just go with the first lender you talk to. Shop around and get quotes from at least three to five different lenders (banks, credit unions, mortgage brokers). Interest rates and fees can vary significantly, potentially saving you thousands of dollars over the life of the loan. Do this within a short window (e.g., 14-45 days) to minimize the impact on your credit score.

Conclusion: Your Path to Homeownership in 2026

The journey to homeownership in the 2026 housing market, while challenging, is entirely achievable for well-prepared first-time buyers. By focusing on building a strong financial foundation, understanding the various financing options, and leveraging expert advice, you can navigate the market with confidence.

Remember, homeownership is a marathon, not a sprint. It requires careful planning, diligent saving, and a clear understanding of both the upfront and ongoing costs. Start early, educate yourself, and don’t hesitate to seek guidance from financial advisors and real estate professionals. With the right strategies in place, your dream of owning a home in 2026 can become a reality, offering not just a place to live, but a significant step towards long-term financial security and personal fulfillment.