Roth IRA vs. Traditional IRA 2026: Choosing Your Retirement Path

Roth IRA vs. Traditional IRA 2026: Choosing Your Retirement Path

Planning for retirement is one of the most crucial financial decisions an individual will ever make. As we look ahead to 2026, understanding the differences between a Roth IRA and a Traditional IRA becomes even more vital. These two powerful retirement savings vehicles offer distinct advantages, primarily centered around their tax treatment, and choosing the right one can significantly impact your financial well-being in your golden years. This comprehensive guide will delve deep into the intricacies of the Roth IRA vs. Traditional IRA for 2026, helping you navigate the options and make an informed decision that aligns with your personal financial goals and future tax expectations.

The landscape of retirement planning is constantly evolving, with economic factors, legislative changes, and personal circumstances all playing a role. Consequently, what might be the best choice for one individual could be detrimental for another. Our aim is to provide a detailed, accessible comparison, highlighting the key features, benefits, and considerations for both the Roth IRA and the Traditional IRA, specifically with a view towards the 2026 tax year and beyond. By the end of this article, you will have a clearer understanding of which IRA might be the optimal choice for your retirement strategy.

Understanding the Fundamentals: What is an IRA?

Before we dissect the differences between a Roth IRA and a Traditional IRA, it’s essential to understand what an Individual Retirement Arrangement (IRA) is at its core. An IRA is a tax-advantaged savings plan that allows individuals to save for retirement with tax-deferred growth or tax-free withdrawals, depending on the type of IRA. The primary benefit of IRAs is the incentive they provide for long-term savings, encouraging individuals to build a substantial nest egg for their post-working life.

Both Roth and Traditional IRAs offer a broad range of investment options, including stocks, bonds, mutual funds, and exchange-traded funds (ETFs). This flexibility allows investors to tailor their portfolios to their risk tolerance and financial objectives. The annual contribution limits for IRAs are set by the IRS and are subject to change. For 2026, it’s crucial to stay updated on these limits, as they dictate how much you can contribute each year. These limits typically include a standard contribution amount and an additional catch-up contribution for those aged 50 and over, recognizing the need for accelerated savings later in life.

The power of compound interest is a significant advantage of investing in an IRA. By allowing your investments to grow untouched over decades, even small contributions can accumulate into substantial sums. This long-term growth, coupled with the tax advantages, makes IRAs an indispensable tool in any comprehensive retirement plan. Now, let’s explore the distinct characteristics of the Roth IRA vs. Traditional IRA for 2026.

Traditional IRA: The "Tax Now, Deduct Later" Approach

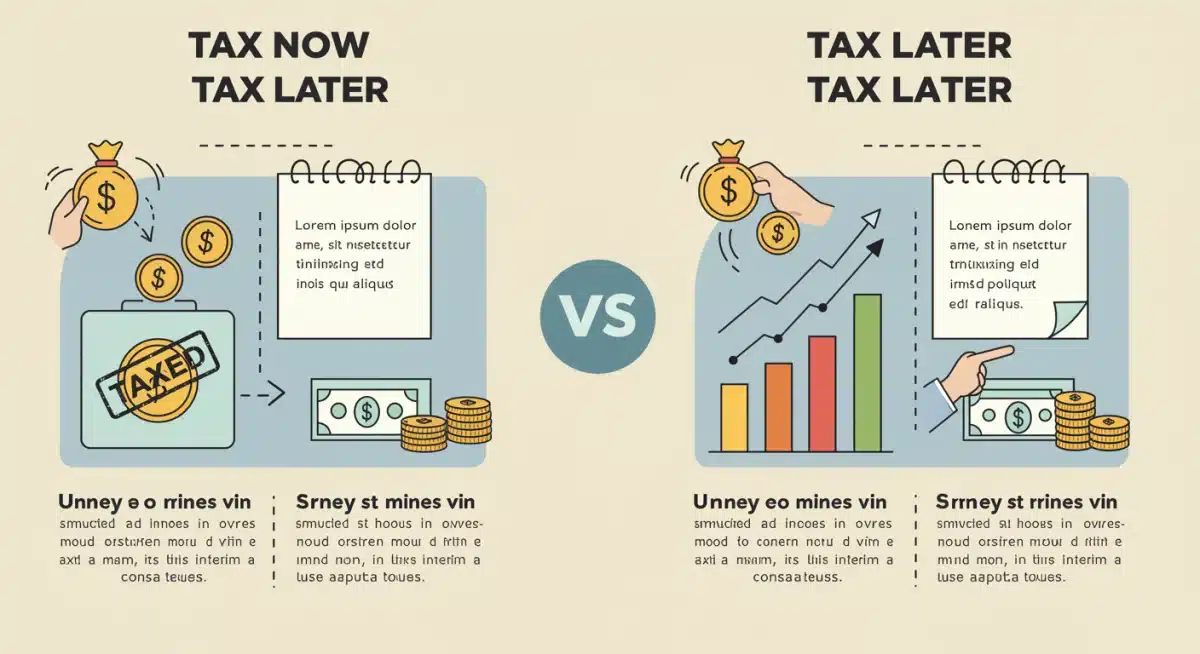

The Traditional IRA is often considered the classic retirement savings vehicle, offering immediate tax benefits for many contributors. The defining characteristic of a Traditional IRA is that contributions are often tax-deductible in the year they are made. This means that if you contribute to a Traditional IRA, you can reduce your taxable income for that year, potentially lowering your current tax bill. This "tax now, deduct later" approach is particularly appealing to individuals who expect to be in a higher tax bracket during their working years than in retirement.

Key Features of a Traditional IRA:

- Tax-Deductible Contributions: Depending on your income and whether you are covered by a retirement plan at work, your contributions to a Traditional IRA may be fully or partially tax-deductible. This is one of the most significant advantages for those seeking immediate tax relief.

- Tax-Deferred Growth: Your investments grow tax-deferred. This means you don’t pay taxes on any capital gains, dividends, or interest earned until you withdraw the money in retirement. This compounding growth, unhindered by annual taxes, can dramatically increase your overall return.

- Taxable Withdrawals in Retirement: When you start taking distributions from your Traditional IRA in retirement, these withdrawals are taxed as ordinary income. The assumption here is that you will be in a lower tax bracket during retirement, thus paying less in taxes overall.

- Required Minimum Distributions (RMDs): Traditional IRAs are subject to RMDs, which typically begin at age 73 (as per current legislation, though this can change). These are mandatory withdrawals that you must start taking from your account, regardless of whether you need the money, to ensure the IRS eventually collects its tax revenue.

- No Income Limits for Contributions: Unlike Roth IRAs, there are no income limits that prevent you from contributing to a Traditional IRA. However, income limits do apply to the deductibility of contributions if you are also covered by a workplace retirement plan.

Who Benefits Most from a Traditional IRA?

A Traditional IRA is often the preferred choice for individuals who:

- Are currently in a higher tax bracket and anticipate being in a lower tax bracket during retirement.

- Want to reduce their current taxable income.

- Are self-employed or do not have access to a workplace retirement plan.

- Are above the income limits for contributing to a Roth IRA.

The immediate tax deduction can be a powerful incentive, especially for those who are focused on minimizing their current tax burden. However, the future tax liability on withdrawals is a critical consideration. Understanding the Roth Traditional IRA 2026 landscape requires a clear grasp of these immediate versus deferred tax benefits.

Roth IRA: The "Tax Later, Withdraw Tax-Free" Approach

The Roth IRA stands in stark contrast to its Traditional counterpart, offering a unique set of advantages that appeal to a different demographic of savers. The defining feature of a Roth IRA is that contributions are made with after-tax dollars. This means you don’t get an upfront tax deduction for your contributions. However, the significant payoff comes in retirement: qualified withdrawals are entirely tax-free.

Key Features of a Roth IRA:

- Non-Deductible Contributions: Contributions to a Roth IRA are made with money you’ve already paid taxes on. There is no immediate tax deduction for these contributions.

- Tax-Free Growth and Withdrawals: This is the Roth IRA’s most compelling feature. Your investments grow tax-free, and qualified withdrawals in retirement are also tax-free. This means that all the earnings your investments generate over decades are yours to keep, without paying a penny in federal income tax (and usually state income tax, too, depending on your state).

- Income Limits for Contributions: Unlike Traditional IRAs, there are income limitations that determine who can contribute directly to a Roth IRA. These limits are adjusted annually for inflation. For 2026, it will be crucial to check the updated IRS guidelines to see if your modified adjusted gross income (MAGI) falls within the allowable range.

- No Required Minimum Distributions (RMDs) for the Original Owner: A significant advantage of the Roth IRA is that the original owner is not subject to RMDs during their lifetime. This offers greater flexibility in managing your retirement income and allows your money to continue growing tax-free for as long as you live. Beneficiaries, however, may be subject to RMDs.

- Access to Contributions Anytime, Tax-Free and Penalty-Free: You can withdraw your original contributions (not earnings) from a Roth IRA at any time, tax-free and penalty-free. This provides a degree of liquidity that Traditional IRAs do not offer, making it a valuable emergency fund or a source for specific financial goals before retirement, though it’s generally not recommended to tap into retirement savings prematurely.

Who Benefits Most from a Roth IRA?

A Roth IRA is often the ideal choice for individuals who:

- Are currently in a lower tax bracket and anticipate being in a higher tax bracket during retirement.

- Are young and have many years for their investments to grow tax-free.

- Value the certainty of tax-free income in retirement.

- Want to avoid RMDs as the original owner.

- May need access to their contributions before retirement without penalty.

The long-term benefit of tax-free withdrawals can be incredibly powerful, especially for those who foresee higher tax rates in the future or who are just starting their careers and have decades of tax-free growth ahead. Considering the Roth Traditional IRA 2026 options, the Roth IRA offers a compelling proposition for future tax certainty.

Roth IRA vs. Traditional IRA 2026: A Head-to-Head Comparison

Now that we’ve covered the individual characteristics of each, let’s put the Roth IRA vs. Traditional IRA side-by-side for 2026 to highlight their key differences and help you decide.

Tax Treatment: Now vs. Later

- Traditional IRA: Contributions are often tax-deductible in the current year, reducing your taxable income. Withdrawals in retirement are taxed as ordinary income. This is advantageous if you expect to be in a lower tax bracket in retirement.

- Roth IRA: Contributions are made with after-tax dollars and are not deductible. Qualified withdrawals in retirement are completely tax-free. This is beneficial if you expect to be in a higher tax bracket in retirement or want tax certainty.

Income Limitations:

- Traditional IRA: No income limits for contributing. However, income limits apply to the deductibility of contributions if you are covered by a workplace retirement plan.

- Roth IRA: Has modified adjusted gross income (MAGI) limits for direct contributions. If your income exceeds these limits, you may still be able to contribute via the "backdoor Roth IRA" strategy.

Withdrawal Rules:

- Traditional IRA: Withdrawals before age 59½ are generally subject to ordinary income tax and a 10% penalty, with some exceptions. Required Minimum Distributions (RMDs) typically begin at age 73.

- Roth IRA: Qualified withdrawals (after age 59½ and after the account has been open for at least five years) are tax-free and penalty-free. Contributions can be withdrawn at any time without tax or penalty. No RMDs for the original owner.

Flexibility and Estate Planning:

- Traditional IRA: Less flexible in terms of early withdrawals due to potential taxes and penalties. RMDs can force distributions you don’t need.

- Roth IRA: Greater flexibility with access to contributions. No RMDs for the original owner means the money can continue to grow tax-free and be passed on to beneficiaries as a tax-free inheritance (though beneficiaries will have RMDs). This makes the Roth IRA a powerful estate planning tool.

Backdoor Roth IRA: A Strategy for High Earners

For individuals whose income exceeds the Roth IRA contribution limits, the "backdoor Roth IRA" strategy remains a popular and legitimate way to get money into a Roth account. This strategy involves contributing non-deductible funds to a Traditional IRA and then immediately converting those funds to a Roth IRA. While the conversion itself is a taxable event if there are any pre-tax dollars in the Traditional IRA, if the contribution was non-deductible, the conversion of that principal amount is typically tax-free.

It’s crucial to understand the "pro-rata rule" when implementing a backdoor Roth IRA. This rule dictates that if you have any other pre-tax Traditional IRA balances (including SEP IRAs or SIMPLE IRAs), a portion of your conversion will be taxable. This can complicate the strategy and potentially lead to an unexpected tax bill. Consulting a tax professional is highly recommended before attempting a backdoor Roth IRA, especially if you have existing pre-tax IRA accounts.

The viability of the backdoor Roth IRA for 2026 depends on current tax laws. While it has been in place for several years, legislative changes are always a possibility. Staying informed about any potential modifications to tax codes is essential for anyone considering this strategy.

Roth 401(k) vs. Traditional 401(k) vs. IRA: Expanding Your Retirement Toolkit

While this article focuses on the Roth IRA vs. Traditional IRA for 2026, it’s worth briefly touching upon their workplace counterparts: the Roth 401(k) and Traditional 401(k). Many employers offer these options, and understanding how they interact with IRAs is crucial for a holistic retirement plan.

- Traditional 401(k): Similar to a Traditional IRA, contributions are pre-tax (reducing current taxable income), grow tax-deferred, and withdrawals in retirement are taxed as ordinary income. Contribution limits are significantly higher than IRAs.

- Roth 401(k): Similar to a Roth IRA, contributions are after-tax, grow tax-free, and qualified withdrawals in retirement are tax-free. Also has higher contribution limits than IRAs.

If you have access to both a workplace plan (like a 401(k)) and an IRA, you can often contribute to both, maximizing your tax-advantaged savings. The decision between a Roth or Traditional version for your 401(k) will follow similar logic to your IRA decision, primarily based on your current and anticipated future tax brackets. For 2026, many individuals will find themselves contributing to both types of accounts to diversify their tax exposure in retirement.

Making the Right Choice for 2026: Key Considerations

Choosing between a Roth IRA and a Traditional IRA for 2026 is a highly personal decision that should be based on several factors. There’s no one-size-fits-all answer, but by carefully evaluating your circumstances, you can make the choice that best supports your financial future.

1. Your Current vs. Future Tax Bracket:

- If you expect your tax bracket to be higher in retirement than it is now: A Roth IRA is generally more advantageous. You pay taxes now at a lower rate, and enjoy tax-free withdrawals later when you’re in a higher bracket.

- If you expect your tax bracket to be lower in retirement than it is now: A Traditional IRA might be better. You get a tax deduction now when you’re in a higher bracket, and pay taxes later when you’re in a lower bracket.

This is arguably the most critical factor in the Roth IRA vs. Traditional IRA debate. Consider your career trajectory, anticipated income growth, and potential changes to tax laws when making this assessment for 2026.

2. Income Levels and Eligibility:

- Check the IRS income limits for direct Roth IRA contributions for 2026. If you exceed them, consider the backdoor Roth IRA strategy.

- For Traditional IRAs, consider if your contributions will be deductible based on your income and workplace retirement plan coverage.

Eligibility is a practical constraint that will immediately narrow down your options. Be sure to verify the precise income thresholds for Roth IRA 2026 contributions.

3. Access to Funds Before Retirement:

- If you anticipate needing to access your contributions before retirement age (e.g., for a down payment on a first home, or other emergencies), a Roth IRA offers more flexibility since you can withdraw your contributions tax-free and penalty-free.

- Traditional IRA withdrawals before 59½ are generally subject to taxes and penalties, making it less suitable for pre-retirement access.

4. Estate Planning Goals:

- If leaving a tax-free inheritance to beneficiaries is a priority, a Roth IRA is superior due to its tax-free withdrawal nature for beneficiaries (though they will have RMDs).

- Traditional IRAs passed to beneficiaries will be subject to income tax upon withdrawal.

5. Age and Time Horizon:

- Younger investors with many years until retirement often benefit more from a Roth IRA, as the tax-free growth has decades to compound.

- Those closer to retirement might find the immediate tax deduction of a Traditional IRA more appealing, especially if their income is currently high.

6. Diversifying Your Tax Exposure:

Many financial advisors recommend a hybrid approach, contributing to both pre-tax (Traditional) and after-tax (Roth) accounts. This strategy provides tax diversification, hedging against future uncertainty regarding tax rates. By having both taxable and tax-free income streams in retirement, you gain greater control over your taxable income in any given year, allowing for more strategic withdrawal planning. This is an increasingly popular approach for prudent retirement savers looking at the Roth Traditional IRA 2026 options.

The Impact of Potential Tax Law Changes in 2026

It’s important to remember that tax laws are not static. While we are planning for 2026, there could be legislative changes that impact the rules surrounding IRAs. Historically, Congress has debated and sometimes enacted changes to contribution limits, income thresholds, RMD rules, and even the existence of certain retirement account types. Staying informed about potential tax law changes is crucial for optimizing your retirement strategy.

For instance, discussions around tax rates can heavily influence the Roth vs. Traditional decision. If future tax rates are projected to increase significantly, the Roth IRA’s tax-free withdrawals become even more valuable. Conversely, if tax rates are expected to fall, the Traditional IRA’s upfront deduction might be more appealing. While we can’t predict the future with certainty, making educated guesses based on current economic and political trends can help inform your decision for the Roth Traditional IRA 2026.

Consulting a Financial Advisor

Given the complexity and personalized nature of retirement planning, consulting a qualified financial advisor is highly recommended. A professional can help you:

- Assess your current financial situation, income, and long-term goals.

- Project your future tax brackets based on your career and retirement plans.

- Navigate the nuances of income limits, deductibility rules, and RMDs.

- Develop a comprehensive retirement strategy that incorporates both IRAs and other retirement vehicles.

- Stay updated on any changes to tax laws that might affect your chosen strategy for 2026 and beyond.

Their expertise can provide clarity and confidence in your retirement planning decisions, ensuring you choose the best path for your unique circumstances.

Conclusion: Your Retirement, Your Choice for 2026

The decision between a Roth IRA and a Traditional IRA for 2026 is a pivotal one that can significantly shape your financial future. Both offer powerful tax advantages, but they cater to different financial situations and future tax expectations. The Traditional IRA provides immediate tax deductions and tax-deferred growth, with withdrawals taxed in retirement. The Roth IRA offers no upfront deduction but promises tax-free growth and tax-free withdrawals in retirement.

By carefully evaluating your current income, anticipated future tax bracket, need for liquidity, and estate planning goals, you can determine which IRA aligns best with your objectives. Remember that it’s not always an either/or situation; many individuals benefit from contributing to both types of accounts to achieve tax diversification. As you plan for 2026 and the years beyond, staying informed, assessing your personal circumstances, and seeking professional advice will empower you to build a robust and tax-efficient retirement nest egg. The Roth Traditional IRA 2026 choice is yours to make, and with careful consideration, it can lead to a more secure and prosperous retirement.

Limits")

Contributions 2026: High Earners' Ultimate Guide")