Capital Gains Taxes 2026: Investor’s Essential Guide

Understanding Capital Gains Taxes in 2026: A Guide for Investors

As an investor, navigating the complex world of taxes is an inescapable part of managing your portfolio. Among the many tax considerations, capital gains taxes stand out as a critical area that can significantly impact your net returns. With the ever-evolving tax landscape, staying informed about current and future regulations is paramount. This comprehensive guide is designed to shed light on capital gains 2026, providing investors with the essential knowledge needed to understand, plan for, and potentially mitigate their tax liabilities.

The year 2026 is particularly significant due to potential legislative changes and the sunsetting of certain provisions from the Tax Cuts and Jobs Act (TCJA) of 2017. These impending shifts could redefine how investment gains are taxed, making proactive planning more important than ever. Whether you’re a seasoned investor or just starting, a clear understanding of capital gains taxes will empower you to make more informed investment decisions and optimize your financial outcomes.

What Are Capital Gains? A Fundamental Review

Before diving into the specifics of capital gains 2026, let’s establish a foundational understanding of what capital gains are. Simply put, a capital gain is the profit you make from selling an asset that has increased in value. These assets can include stocks, bonds, real estate, collectibles, and even certain types of personal property. The difference between the asset’s selling price and its original purchase price (known as its basis) is your capital gain.

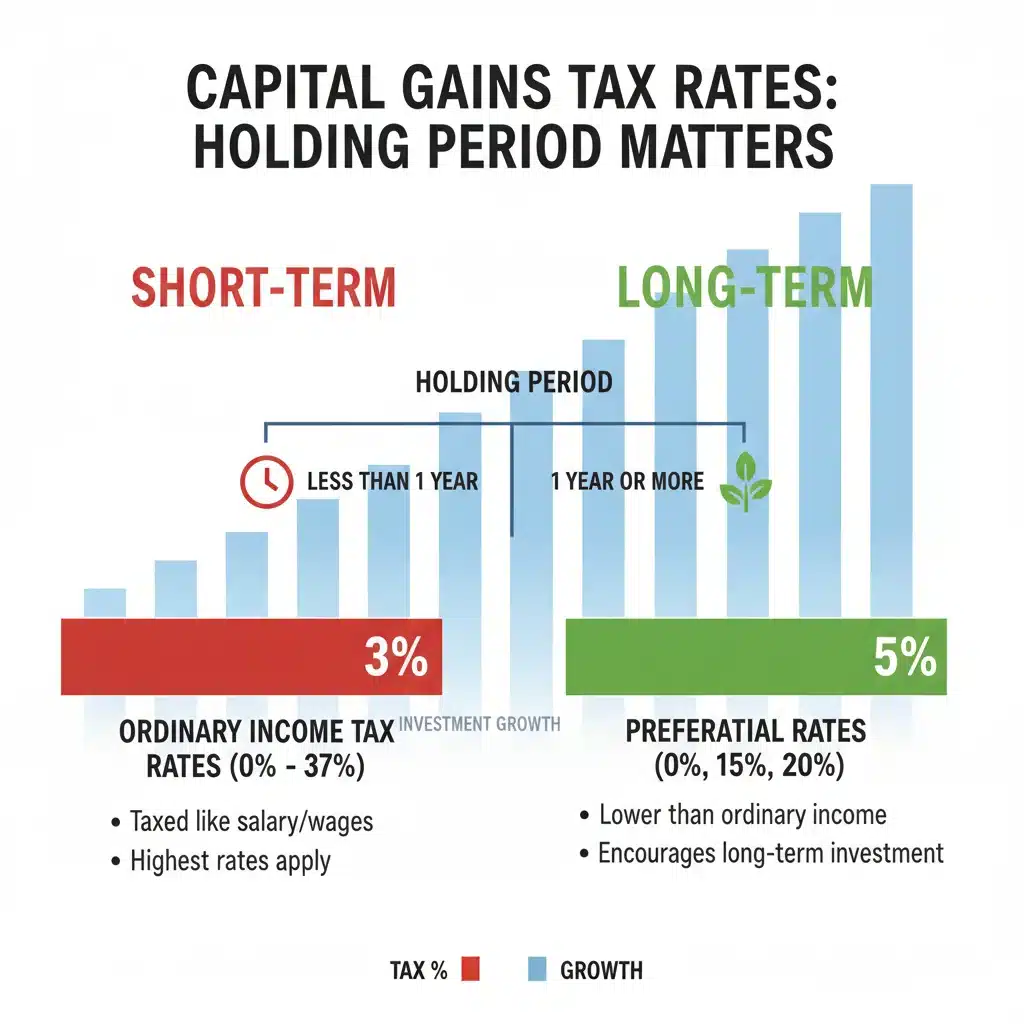

Not all capital gains are treated equally by the IRS. The duration for which you hold an asset before selling it is a crucial determinant of how your gain will be taxed. This distinction leads to two primary categories of capital gains:

- Short-Term Capital Gains: These are profits from assets held for one year or less. Short-term capital gains are typically taxed at your ordinary income tax rates, which can be significantly higher than long-term rates.

- Long-Term Capital Gains: These are profits from assets held for more than one year. Long-term capital gains usually qualify for preferential tax rates, which are often lower than ordinary income tax rates.

Understanding this fundamental difference is the first step in effective tax planning for your investments. The holding period is calculated from the day after you acquire the asset to the day you sell it. For example, if you buy a stock on January 15, 2025, and sell it on January 15, 2026, it’s considered a short-term gain. If you sell it on January 16, 2026, it becomes a long-term gain.

It’s also important to remember that capital losses can offset capital gains. If your capital losses exceed your capital gains, you can deduct up to $3,000 of those losses against your ordinary income in a given year. Any remaining losses can be carried forward to future tax years.

The Current Capital Gains Tax Landscape (Pre-2026 Context)

To fully appreciate the potential changes for capital gains 2026, it’s helpful to review the current tax environment. As of recent years, the long-term capital gains tax rates have been tiered, typically at 0%, 15%, and 20%, depending on your taxable income. These rates are generally lower than the ordinary income tax brackets.

Current Long-Term Capital Gains Tax Rates (Example for 2025 Tax Year)

- 0% Rate: Applies to taxpayers in the lowest income tax brackets. For example, single filers with taxable income up to approximately $47,000, and married couples filing jointly with taxable income up to around $94,000 (these figures are illustrative and subject to annual adjustment).

- 15% Rate: Applies to the majority of taxpayers whose income falls between the 0% and 20% thresholds. For single filers, this might be between $47,001 and $518,000; for married couples filing jointly, between $94,001 and $583,750 (again, illustrative figures).

- 20% Rate: Reserved for high-income earners. For single filers, taxable income above approximately $518,000; for married couples filing jointly, above around $583,750.

Short-term capital gains, as mentioned, are taxed at your ordinary income tax rates, which can range from 10% to 37% (for the highest earners). This significant difference underscores the importance of holding assets for more than one year whenever possible, aligning with sound investment principles of patience and long-term growth.

Beyond these rates, investors must also consider the Net Investment Income Tax (NIIT). This 3.8% tax applies to the lesser of your net investment income or the amount by which your modified adjusted gross income (MAGI) exceeds certain thresholds ($200,000 for single filers, $250,000 for married filing jointly). This tax can effectively increase your long-term capital gains rate if your income is high enough.

Understanding these current rules provides a benchmark against which to assess potential changes in 2026. The political and economic climate often dictates tax policy, and upcoming elections and budgetary needs can significantly influence future legislation.

Anticipating Capital Gains Changes in 2026

The year 2026 is poised to be a pivotal year for tax policy, largely due to the scheduled expiration of many provisions from the Tax Cuts and Jobs Act (TCJA) of 2017. While the TCJA primarily focused on individual income tax rates and deductions, its sunsetting could indirectly impact capital gains taxation, especially if new legislation is enacted to replace or modify its provisions. Furthermore, discussions around potential new tax legislation, often driven by shifts in political power, could directly target investment income.

Potential Scenarios for Capital Gains 2026:

- Expiration of TCJA Provisions: If no new legislation is passed, many individual tax provisions are set to revert to pre-TCJA levels. While capital gains rates were not directly altered by the TCJA in the same way ordinary income rates were, the overall tax brackets and thresholds could shift. This means that the income levels at which the 0%, 15%, and 20% long-term capital gains rates apply could change, potentially pushing more taxpayers into higher capital gains brackets even if the rates themselves remain numerically the same.

- Proposals for Higher Capital Gains Taxes: There have been ongoing discussions and proposals from various political factions to increase capital gains taxes, particularly for high-income earners. Some proposals have suggested taxing long-term capital gains at ordinary income rates for individuals above certain income thresholds. This would be a significant shift, as it would effectively eliminate the preferential treatment for long-term investments for a segment of the population.

- Wealth Taxes or Mark-to-Market Rules: While less likely to be implemented broadly by 2026, some progressive proposals have included ideas like annual wealth taxes or ‘mark-to-market’ taxation, where unrealized gains on certain assets would be taxed annually. These are more radical changes but highlight the potential direction of future tax policy discussions.

- Status Quo (Unlikely but Possible): It’s also possible, though less probable given the political landscape, that the existing capital gains tax structure remains largely unchanged. However, even in this scenario, inflation adjustments to income thresholds would still occur.

Investors should pay close attention to political developments, especially leading up to and following the 2024 elections, as these will likely determine the legislative agenda for 2025 and 2026. Any major tax reform could have a profound impact on investment strategies and financial planning.

Key Tax Planning Strategies for Capital Gains 2026

Given the potential for changes in capital gains 2026, proactive tax planning is more crucial than ever. Here are several strategies investors can employ to optimize their tax situation and potentially mitigate future liabilities:

1. Harvest Capital Losses

Capital loss harvesting is a powerful strategy that involves selling investments at a loss to offset capital gains. As mentioned earlier, you can use capital losses to offset an unlimited amount of capital gains and then deduct up to $3,000 of net capital losses against your ordinary income each year. Any unused losses can be carried forward indefinitely to future tax years.

This strategy is particularly effective when you have significant gains in your portfolio. By strategically selling losing positions, you can reduce your overall taxable income. However, be mindful of the wash-sale rule, which prevents you from buying substantially identical securities within 30 days before or after selling them at a loss. Planning your loss harvesting carefully can significantly improve your after-tax returns.

2. Optimize Holding Periods

The distinction between short-term and long-term capital gains is paramount. Whenever possible, aim to hold appreciated assets for more than one year to qualify for the more favorable long-term capital gains rates. This simple act can lead to substantial tax savings, especially for investors in higher income brackets. Before selling any asset, always check its holding period to understand the tax implications.

3. Utilize Tax-Advantaged Accounts

Maximizing contributions to tax-advantaged accounts like 401(k)s, IRAs (Traditional and Roth), and Health Savings Accounts (HSAs) can be an excellent way to defer or even avoid capital gains taxes. Investments within these accounts grow tax-deferred or tax-free, meaning you don’t pay capital gains taxes on transactions within the account until withdrawal (for tax-deferred accounts like Traditional IRAs and 401(k)s), or you pay no taxes on qualified withdrawals at all (for Roth accounts and HSAs).

Even if you anticipate higher capital gains rates in 2026, contributing to these accounts provides a shield against immediate taxation on your investment growth, allowing your money to compound more effectively.

4. Consider Tax-Efficient Investments

Certain investment vehicles are inherently more tax-efficient. For instance, municipal bonds often offer tax-exempt interest income at the federal level, and sometimes at the state and local levels too, depending on where you live and where the bond was issued. Exchange-Traded Funds (ETFs) are generally more tax-efficient than actively managed mutual funds because their structure often results in fewer capital gains distributions to shareholders.

Also, consider investments that generate qualified dividends, which are often taxed at the same preferential rates as long-term capital gains.

5. Gifting Appreciated Assets

If you plan to make charitable donations, consider gifting appreciated securities instead of cash. If you donate stock you’ve held for more than a year to a qualified charity, you can typically deduct the fair market value of the stock (up to certain limits) and avoid paying capital gains tax on the appreciation. The charity, being tax-exempt, also avoids paying capital gains tax when they sell the stock.

Similarly, if you plan to gift assets to family members, gifting appreciated assets (especially to those in lower tax brackets) can be a strategic move. However, be aware of gift tax rules and the donor’s basis carryover. Consulting with a tax professional is highly recommended for these strategies.

6. Qualified Opportunity Zones (QOZs)

Qualified Opportunity Zones offer significant tax incentives for investing in designated economically distressed communities. By reinvesting eligible capital gains into a Qualified Opportunity Fund (QOF), investors can defer, reduce, and potentially eliminate capital gains taxes on the original gain, as well as on any new gains from the QOF investment itself, if held for a sufficient period. While these investments come with their own risks and complexities, they can be a powerful tool for certain investors looking to defer or reduce future capital gains.

7. Retirement Planning and Required Minimum Distributions (RMDs)

As you approach retirement, understanding how RMDs from tax-deferred accounts impact your taxable income is crucial. Higher taxable income can push you into higher capital gains brackets if you also realize significant gains from your taxable accounts. Strategic Roth conversions in years with lower income or before expected increases in tax rates can help manage future tax liabilities, including those related to capital gains.

The Role of Professional Advice in Navigating Capital Gains 2026

While this guide provides a comprehensive overview, the nuances of tax law and personal financial situations are complex. The potential changes in capital gains 2026 make the expertise of a qualified financial advisor or tax professional invaluable. A professional can:

- Assess Your Unique Situation: They can analyze your specific financial goals, income level, and investment portfolio to tailor tax strategies that are most beneficial for you.

- Stay Updated on Legislation: Tax laws are constantly changing. A professional will be up-to-date on the latest legislative developments and interpret how they apply to your investments.

- Identify Opportunities and Risks: They can help you uncover tax-saving opportunities you might miss and warn you about potential pitfalls or unintended consequences of certain actions.

- Ensure Compliance: Navigating tax forms and regulations can be daunting. A professional ensures you comply with all IRS rules, avoiding costly errors or penalties.

- Long-Term Planning: They can help you integrate capital gains tax planning into your broader financial plan, including retirement, estate planning, and wealth transfer strategies.

Engaging with a professional can provide peace of mind and, more importantly, lead to significant tax savings over the long term, especially as we approach a potentially transformative year like 2026 for capital gains taxation.

Beyond Capital Gains: Other Tax Considerations for Investors

While the focus of this guide is capital gains 2026, it’s important to remember that investment income encompasses more than just capital gains. Investors also need to consider:

- Dividends: These are distributions of profits by corporations to their shareholders. Qualified dividends are taxed at the same preferential rates as long-term capital gains, while non-qualified (ordinary) dividends are taxed at ordinary income rates.

- Interest Income: Earned from bonds, savings accounts, and other debt instruments. This is generally taxed at ordinary income rates, with the exception of certain municipal bond interest.

- Rental Income: If you own investment properties, rental income is typically taxed as ordinary income, though it comes with various deductions for expenses, depreciation, and sometimes passive activity loss rules.

- Alternative Minimum Tax (AMT): The AMT is a separate tax system designed to ensure that high-income taxpayers pay a minimum amount of tax, regardless of deductions and credits. While its impact has lessened for many under TCJA, it’s still a consideration for some investors, as it can affect how certain deductions and preferential tax treatments are applied.

A holistic approach to tax planning considers all sources of investment income and how they interact with your overall tax liability. The strategies discussed for capital gains can often be adapted or complemented by strategies for other types of investment income.

The Economic and Political Context Leading to 2026

The trajectory of tax policy is rarely set in stone and is heavily influenced by the prevailing economic conditions and political landscape. As we look towards 2026, several factors could shape the final outcome of capital gains taxation:

- Inflation and Interest Rates: Persistent inflation and rising interest rates can influence investment returns and, consequently, the amount of capital gains realized by investors. Policymakers might consider tax changes as part of broader economic stimulus or stabilization efforts.

- National Debt: The growing national debt often prompts discussions about increasing tax revenues. Capital gains taxes, especially on high earners, are frequently targeted as a potential source of additional government funds.

- Political Climate: The outcome of federal elections in 2024 will be a major determinant. A shift in presidential administration or congressional control could lead to significant changes in tax philosophy and legislative priorities, directly impacting capital gains 2026.

- Wealth Inequality: Debates surrounding wealth inequality often bring investment income, including capital gains, into focus. Proposals aimed at addressing wealth disparities commonly include higher taxes on capital gains for the wealthiest individuals.

Investors should remain vigilant and informed about these macroeconomic and political developments. While you cannot control these external factors, understanding their potential influence allows for more agile and responsive financial planning.

Conclusion: Preparing for Capital Gains 2026

The landscape of capital gains taxation is dynamic, with 2026 representing a potential inflection point due to the sunsetting of TCJA provisions and ongoing policy debates. For investors, this means that complacency is not an option. A proactive and informed approach to understanding and planning for capital gains 2026 is essential for protecting and growing your wealth.

By reviewing the fundamentals of capital gains, understanding the current tax environment, anticipating potential changes, and implementing smart tax planning strategies, you can position yourself to navigate the future tax landscape effectively. Remember the power of loss harvesting, optimizing holding periods, leveraging tax-advantaged accounts, and considering tax-efficient investments. Most importantly, don’t hesitate to seek the guidance of a qualified tax professional or financial advisor to tailor these strategies to your unique circumstances.

Staying informed, planning ahead, and adapting to change will be your greatest assets as you manage your investments and confront the challenges and opportunities presented by capital gains taxes in 2026 and beyond. Your financial future depends on your ability to not just grow your investments, but also to retain as much of that growth as possible after taxes.

Limits")